Adobe’s quarterly results show that its subscription model continues to generate revenue effectively and provides relatively stable growth. At the same time, concerns are growing that sustaining this growth could become challenging amid increasing competition and the emergence of new AI models. Markets are now asking whether Adobe can maintain its edge in the SaaS sector and how the departure of its long-standing CEO will affect the company’s strategic direction and pace of development.

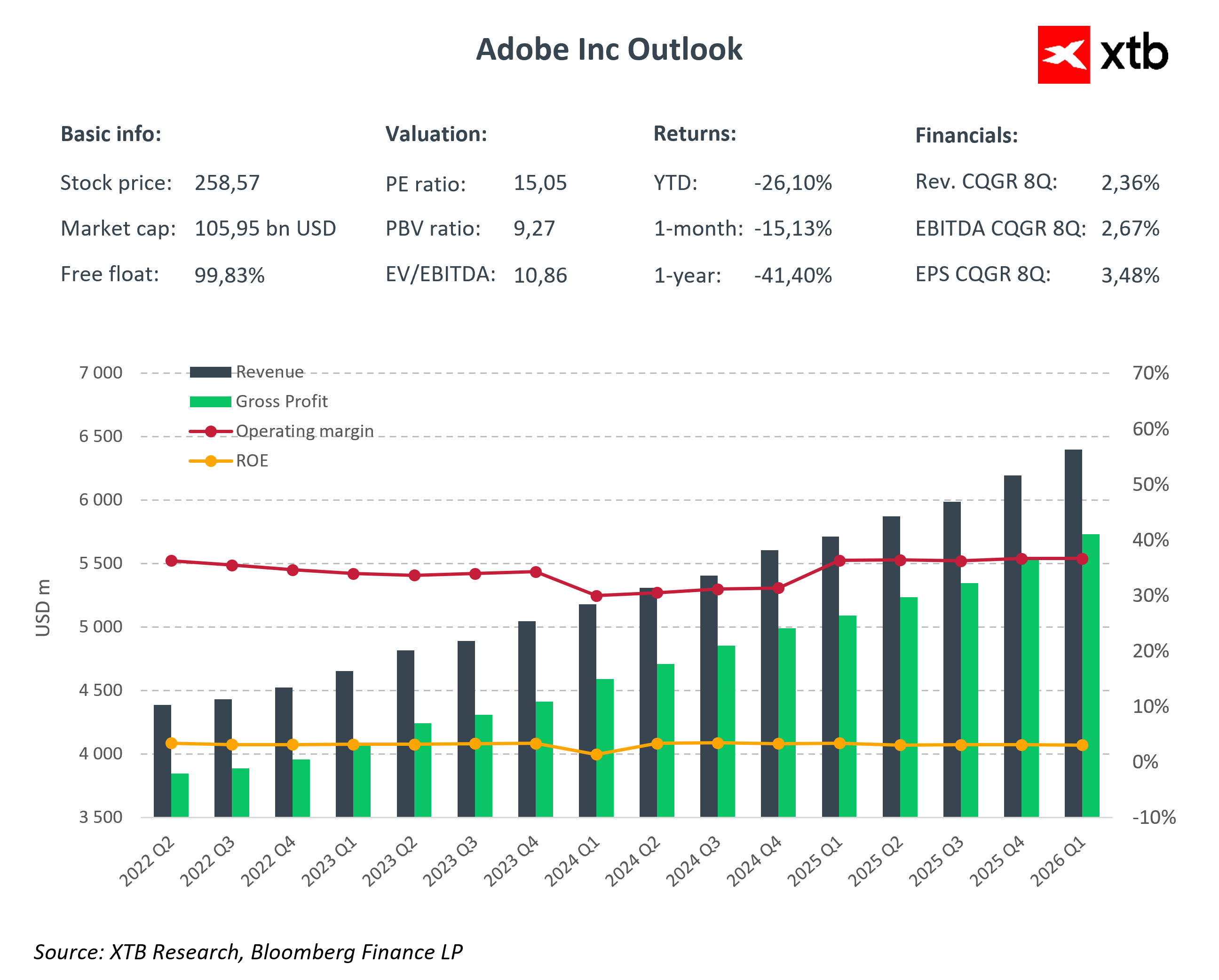

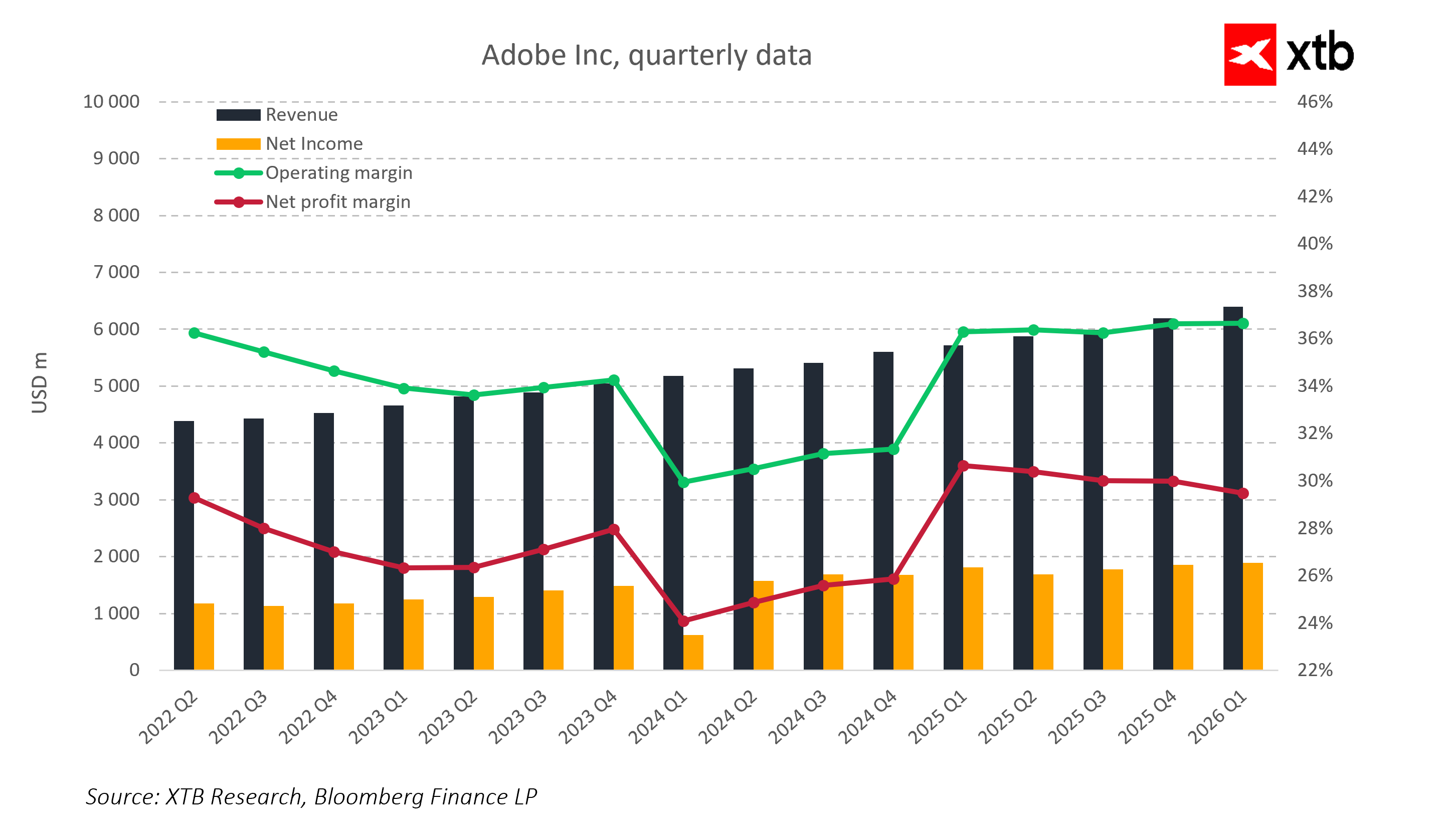

Adobe reported its results for the first quarter of fiscal year 2026, clearly demonstrating growth across key business segments. Revenue reached approximately 6.40 billion USD, representing a 12 percent year-over-year increase and surpassing analysts’ consensus of 6.28 billion USD. Non-GAAP earnings per share came in at 6.06 USD versus an expected 5.87 USD, and the company’s operating cash flow reached a record 2.96 billion USD. These results confirm that subscriptions and dynamically developed AI products, including solutions from the Creative Cloud and Document Cloud, continue to provide solid financial foundations and steadily growing revenue.

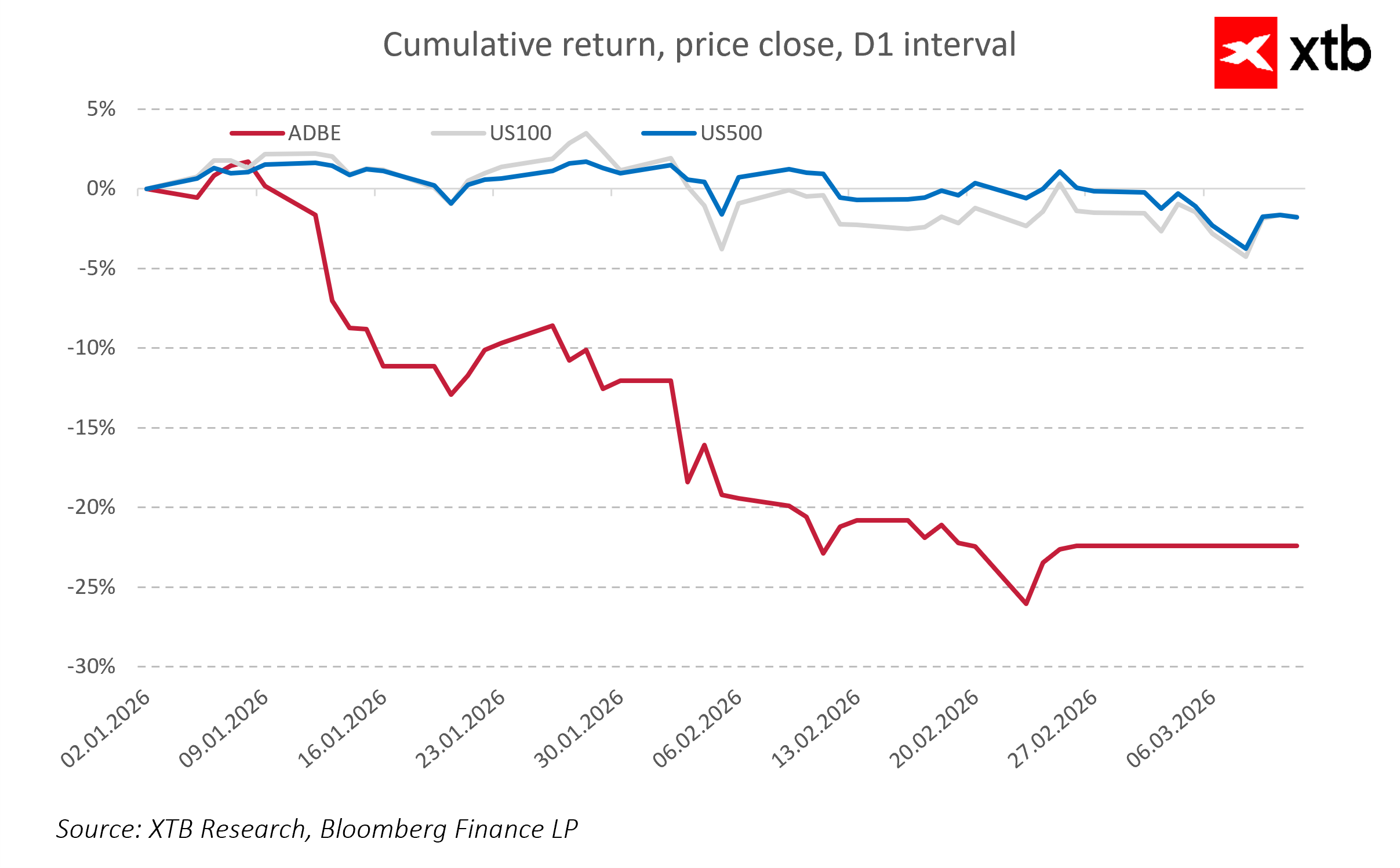

At the same time, the market reacted with a 7-8 percent decline in Adobe’s stock after the close, primarily due to Shantanu Narayen’s announced departure as CEO after eighteen years of leading the company and guiding its transformation toward SaaS and AI-focused products. In a moment when markets are closely analyzing AI’s impact on SaaS companies, this leadership change increases uncertainty regarding the pace of future growth and the effectiveness of strategic initiatives, as well as the CEO’s own confidence in the company’s future.

Adobe highlighted that in the coming quarters, margin pressure is expected to intensify with the emergence of new AI models, which, combined with the departure of its long-standing CEO, helps explain the market’s negative reaction. Investors note that the company faces the challenge not only of sustaining revenue growth but also of managing profitability in an increasingly competitive and dynamic technological environment.

Key Financial Results Q1 FY26

- Revenue: 6.40 billion USD, +12% YoY, above market consensus of 6.28 billion USD

- EPS (non-GAAP): 6.06 USD vs. expected 5.87 USD

- Annual Recurring Revenue and subscription revenues growing, particularly in AI and Creative Cloud segments

- Operating Cash Flow: 2.96 billion USD

Guidance and Risks

Adobe provided a cautious outlook for the coming quarters. For Q2 FY26, revenue is projected in the range of 6.43–6.48 billion USD, with EPS between 5.80–5.85 USD. The market interprets these figures as a signal of caution, indicating that some of the risks related to AI, SaaS competition, and leadership change may materialize.

Key risk factors include margin pressure, as the development and integration of new AI features may increase costs faster than revenues, reducing short-term profitability. The leadership transition following the long-term CEO’s departure at a critical point in the company’s transformation adds uncertainty regarding strategy execution and the effectiveness of AI and SaaS initiatives. In addition, growing competition in AI and SaaS could limit Adobe’s market share, particularly in creative and marketing segments. Despite record-high Annual Recurring Revenue, sustaining subscription growth may become more difficult amid intensifying competition and evolving customer expectations. These risk factors, combined with the cautious guidance for Q2, help explain why Adobe’s stock experienced a significant decline despite record financial results.

Business Segments

Creative Cloud and Document Cloud remain Adobe’s primary revenue drivers, accounting for more than seventy percent of total revenue. This segment is growing 10–13 percent year-over-year, driven by an expanding subscriber base and the implementation of AI-powered features such as Firefly and automation of creative workflows.

Marketing and Experience Cloud, although smaller than the creative segment, shows stable revenue growth but is more sensitive to competition and cost pressures. Rising investment in AI integration and intense competition in the marketing segment make investors approach forecasts cautiously.

AI-first products are contributing to an increasing portion of subscription revenue, and Annual Recurring Revenue has reached record levels, demonstrating the scalability of the SaaS model combined with new AI capabilities. At the same time, the growing number of competitive AI solutions in the SaaS space and concerns over potential value compression for SaaS companies lead the market to price growth more conservatively.

Outlook and Conclusions

Adobe demonstrates that its SaaS model and AI monetization remain solid, providing a foundation for continued revenue growth. The company’s success in the coming quarters will heavily depend on the effective adoption of AI solutions in its products, both in Creative Cloud and Document Cloud, to maintain technological leadership and increase value for customers.

At the same time, the market continues to monitor the impact of the CEO change and the company’s ability to execute its strategy in a rapidly evolving technological environment. Entering the coming quarters, Adobe remains in a phase where financial results are strong, but short-term risks related to leadership, rising AI competition, and margin pressure may lead to greater stock price volatility.

In the long term, Adobe’s fundamentals remain solid, but maintaining a leading position in SaaS and creative technology will largely depend on the successful integration of AI solutions in products and the company’s ability to adapt to growing competition and market changes. Success in this area will determine the continuation of revenue growth and shareholder value.

US OPEN: Cautious gains after GDP disappointment

The End of the Era of Ordinary Memory. Samsung Drives Nvidia’s Future

Why are equities ‘holding up’ in this crisis?

Market wrap: European stocks attempt to stabilize despite the surge in oil prices 🔍

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.