The Australian labour market proved more resilient than expected, with the unemployment rate falling to 4.4% from a five-year high of 4.5%, while employment increased by 40.3k, comfortably beating expectations for a gain of around 30k. At the same time, household spending surprised to the upside, rising 1.3% in May versus market expectations of just 0.5%. For investors, the key takeaway is that the combination of a strong labour market, resilient consumers and still-elevated inflation complicates the case for an early policy easing by the Reserve Bank of Australia (RBA). Money markets continue to price roughly an 80% probability that the RBA will leave interest rates unchanged in August, but the latest data has strengthened the arguments in favour of another rate hike. For the Australian dollar, this provides potential support from a relatively hawkish central bank, although the medium-term direction of the AUD will depend on upcoming inflation and labour market data.

Labour market: Headline numbers beat expectations

The latest figures from the Australian Bureau of Statistics (ABS) showed that the unemployment rate declined to 4.4%, after previously rising to 4.5%, its highest level in five years. This was an important surprise, as economists had expected unemployment to remain unchanged at 4.5%.

Employment increased by 40.3k, significantly outperforming market forecasts. At the same time, around 18.3k people lost their jobs, leaving the overall balance of the labour market firmly positive.

The ABS also noted that the backlog of people waiting to start new jobs eased during May, helping boost employment and reduce unemployment.

One weaker aspect of the report was a 1.1% decline in hours worked. According to the ABS, this was largely due to Australians catching up on leave that had not been taken during April.

At first glance, the report appears very strong: unemployment is falling, employment is rising, and consumers are spending more. These are typically supportive conditions for both the Australian dollar and government bond yields. However, the decline in hours worked and sluggish employment growth over recent quarters suggest the labour market may not be as strong beneath the surface as the headline figures imply. The economy could be approaching a turning point, but it has not reached one yet. For the RBA, the latest data still do not provide sufficient evidence that economic conditions are cooling sustainably.

RBA faces a difficult balancing act

The Reserve Bank of Australia has a dual mandate: maintaining inflation within its 2–3% target range while supporting full employment. The latest economic releases suggest that the Australian economy remains too resilient for the central bank to comfortably shift toward a more dovish stance.

The next set of inflation and labour market data for June will therefore be crucial, as it will represent the final major batch of macroeconomic information before the RBA's August policy meeting.

The RBA recently left its cash rate unchanged at 4.35%, following three consecutive 25-basis-point rate hikes in 2026. Since the beginning of the year, the official cash rate has increased from 3.60% to 4.35%.

For financial markets, the August meeting remains finely balanced. Money markets still assign roughly an 80% probability to a pause, but stronger employment data and the rebound in household spending make such a decision less straightforward.

Inflation remains the key risk

Australia's headline CPI inflation eased to 4.0% YoY in May, down from 4.2% in April. At first glance, this appears to be encouraging news for the RBA.

However, much of the improvement was driven by the Australian government's temporary reduction in fuel excise taxes. Automotive fuel prices declined 11.9% in May, following a 7.0% decline in April.

More importantly, the trimmed mean inflation rate—the RBA's preferred measure of underlying inflation—rose to 3.6% from 3.4%, indicating that underlying price pressures remain persistent after excluding the most volatile components.

For traders, this is the critical part of the inflation story. Unless core inflation begins to decline more convincingly, the RBA may have little choice but to maintain its hawkish rhetoric or even consider another rate increase.

Household spending rebounds

Another important feature of the latest data release was the 1.3% increase in household spending during May. This marked a sharp recovery following declines of 1.1% in April and 1.7% in March.

The figure significantly exceeded expectations of a 0.5% increase, suggesting Australian consumers remain surprisingly resilient despite elevated living costs, higher energy bills and rising mortgage repayments.

Part of the increase reflected the normalisation of airline ticket refunds following disruptions related to the Middle East conflict. Nevertheless, the broader picture remains unchanged: household spending has yet to show signs of a meaningful slowdown.

For the RBA, this creates another challenge. A resilient labour market continues to support household incomes, helping sustain consumption and making it more difficult to return inflation to target.

Mortgage holders remain under pressure

Since the beginning of 2026, the RBA's cash rate has increased from 3.60% to 4.35%. Three consecutive quarter-point rate hikes have added approximately AUD 342 to the average monthly repayment on a typical AUD 736,000 mortgage.

On an annual basis, this translates into roughly AUD 4,128 in additional borrowing costs. Should the RBA deliver a fourth rate increase, Compare the Market estimates average monthly repayments would rise by a further AUD 114.

Combined with the previous hikes, annual mortgage servicing costs would increase by around AUD 5,472. This is particularly important for investors because household finances remain one of the key transmission channels of monetary policy in Australia.

The paradox is that despite mounting pressure on borrowers, consumer spending has yet to weaken materially. This increases the likelihood that the RBA continues to view the economy as too resilient.

Labour shortages remain widespread

Despite record migration levels, Australian businesses continue to report significant labour shortages. According to ABS data, job vacancies remain 45% above pre-pandemic levels and have stayed above 325,000 vacancies for five consecutive years.

The most acute shortages remain in healthcare and social assistance, where vacancies are 90% higher than before the pandemic. Manufacturing vacancies are 78% higher, electricity, gas, water and waste services are 76% above pre-pandemic levels, while mining vacancies remain 58% higher.

This matters because persistent labour shortages tend to keep wage pressures elevated. As long as businesses continue competing for workers, wage inflation could remain stronger than desired even if overall economic growth slows.

For the RBA, this means the labour market may stay too tight for underlying inflation to return quickly to target. For investors, it raises the probability that monetary policy will remain restrictive for longer.

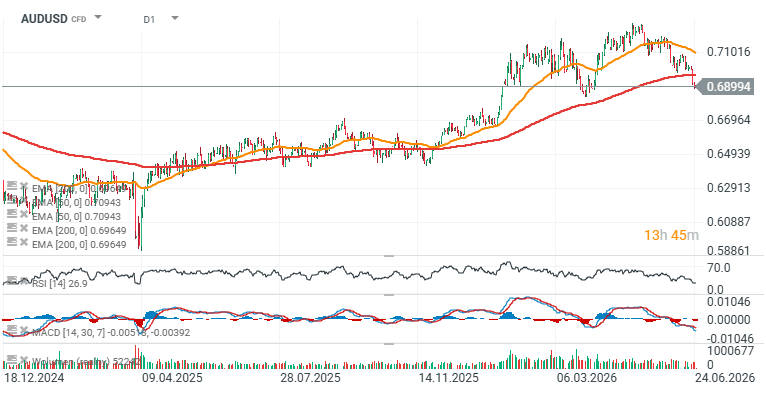

Implications for the Australian dollar – AUD/USD chart

The latest labour market report is broadly supportive for the Australian dollar because it reinforces the case for higher interest rates for longer. Stronger employment, lower unemployment and resilient consumer spending all reduce the scope for the RBA to pivot toward easier monetary policy.

For currency pairs such as AUD/USD, AUD/JPY and EUR/AUD, the key question is whether markets begin shifting expectations from a rate pause toward another hike. If rate hike probabilities continue to increase, the Australian dollar could receive additional support through the interest rate channel.

At the same time, the Australian dollar remains highly sensitive to global risk sentiment, commodity prices and developments in China. Consequently, stronger domestic macroeconomic data alone may not be sufficient to generate a sustained uptrend if global conditions become less supportive for cyclical currencies.

The main conclusion for investors is straightforward: the latest labour market report has reduced expectations of an early dovish shift by the RBA while significantly increasing the importance of the next inflation release.

Looking at the AUD/USD chart, the pair has fallen below the 200-period EMA (red line), which has generally acted as a springboard for rebounds since April 2025. The key question now is whether this latest decline marks the beginning of a more durable trend reversal or simply a deeper correction similar to previous pullbacks. The nearest major support is located around 0.67, corresponding to the March swing lows, while the 200-period EMA near 0.70 now represents the primary resistance level.

Source: xStation5

BREAKING: PCE Inflation and income raise 📈EURUSD gains 0,2%

All eyes on the US, as stocks get a boost from Micron, and the oil price continues to fall

📉 EURUSD below 1.135

Economic calendar 🔼 Markets wait for the key US macro data

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.