European indices are trading lower, with the DAX down more than 0.2%. Investors are assessing the earnings season and awaiting today’s Federal Reserve interest rate decision, as well as results from major US technology companies after the close. US index futures are also slightly lower. The European earnings season has started unevenly, with investors looking for signals on how higher energy prices following the Iran conflict may affect inflation and corporate margins. Europe remains more sensitive to rising oil and gas prices than the US due to its lower domestic energy supply. The market expects that stronger inflationary pressure in Europe could increase the likelihood of a more cautious response from central banks in the coming days.

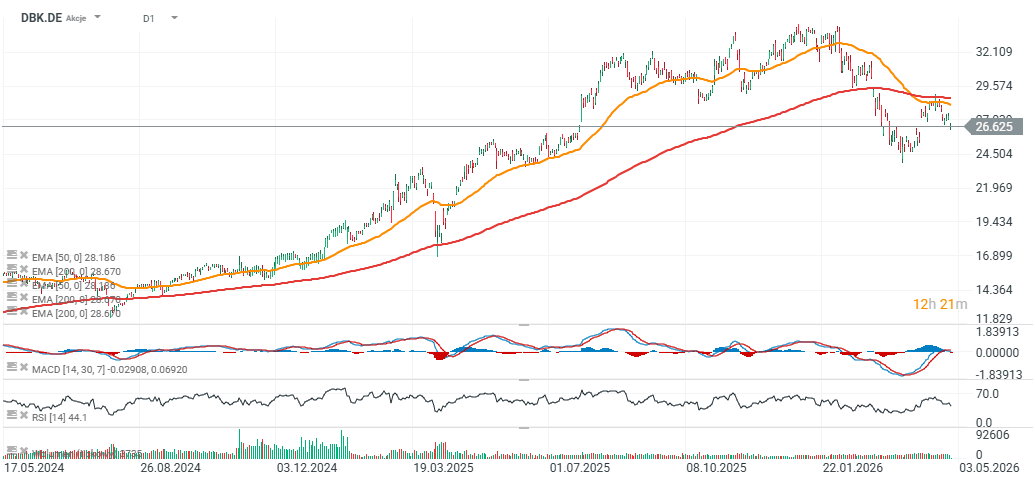

The Stoxx 600 was broadly flat in early trading, reflecting a cautious market tone ahead of key central bank decisions. UBS shares are rising after first-quarter results, supported by strong investment banking activity, which is reinforcing expectations for shareholder payouts. Deutsche Bank declined following concerns related to its exposure to commercial real estate, reminding investors of risks in the banking sector.

Adidas is gaining strongly after better-than-expected quarterly results and reaffirmed full-year guidance, supported by demand for football, running, and training products. Investors are weighing the risk of a prolonged US–Iran conflict against the UAE’s decision to exit OPEC+, which could gradually increase oil supply, although it is unlikely to resolve supply tensions quickly. The weakest sectors in today’s European session include luxury goods, retail, industrials, and utilities.

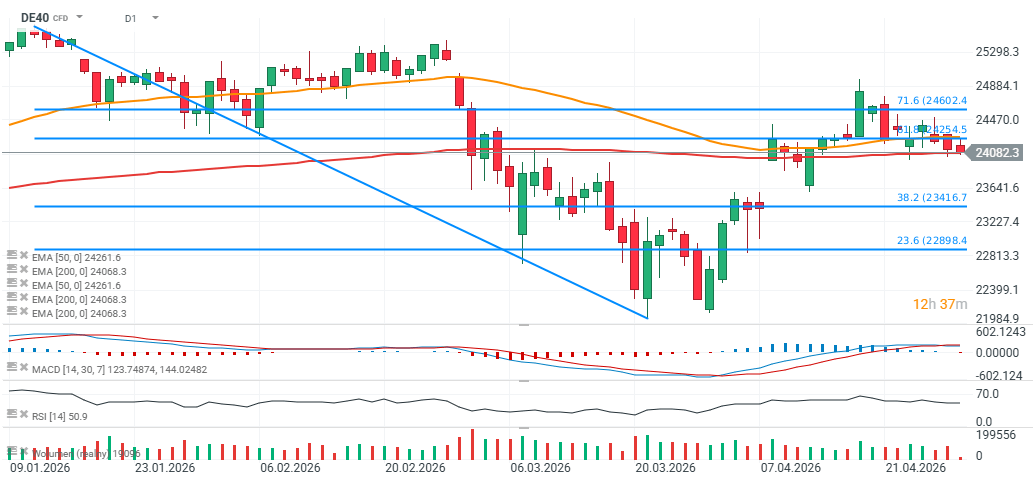

DE40 (D1 timeframe)

Looking at German DAX futures (DE40), prices have pulled back below 4100 points, once again testing the 200-day exponential moving average (EMA200, red line).

Source: xStation5

Oil, inflation and central banks

Oil prices remain elevated, as the market continues to price in the risk of a prolonged blockade involving Iran and potential disruptions to supply from the Persian Gulf region. Inflation risk remains a key factor for bond markets, as higher energy prices can keep pressure on yields and complicate efforts by central banks to ease policy. The Fed is expected to leave rates unchanged, although the market continues to discuss the possibility of future hikes if energy-driven inflation proves persistent.

Currencies and bonds

The US dollar is strengthening amid elevated oil prices, while the euro remains weaker against the dollar. The FX market views the 1.17 level on EUR/USD as a key benchmark for sentiment related to developments in the Middle East. Eurozone bond yields have edged higher ahead of the European Central Bank meeting, and upcoming macroeconomic data may further influence debt market pricing.

Commodities

The oil market remains focused on peace negotiations, developments in the Strait of Hormuz, and US inventory data, which may indicate how quickly stockpiles are declining. Gold is edging lower, although ongoing geopolitical uncertainty continues to support investment demand and central bank purchases. Goldman Sachs maintained a positive outlook on gold, pointing to the potential for prices to reach $5,400 per ounce by year-end.

Key corporate highlights

AstraZeneca is reporting revenue and earnings growth driven by strong sales of oncology and rare disease treatments. Kone has agreed to acquire TK Elevator for approximately $24 billion, a deal that could create the world’s largest elevator manufacturer by sales. GlaxoSmithKline (GSK) improved results thanks to strong specialty medicine sales and announced a higher dividend for 2026. TotalEnergies is increasing shareholder returns, supported by stronger earnings linked to the Middle East conflict.

Santander, Lloyds, and Deutsche Bank have reported improved results, although investors remain focused on credit quality and macro-related risks within the banking sector.

Deutsche Bank (DBK.DE), D1 timeframe

Source: xStation5

Magnificent 7 earnings preview

Chart of the Day: OIL (29.04.2026)

Economic Calendar: Fed Decision, Earnings Reports from Microsoft, Amazon, Meta, and Alphabet

Morning Wrap: A Flurry of Decisions from the Fed and BoC, Plus Q1 Mag7 Earnings ⚡ (29.04.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.